The private health insurance sector is changing faster than ever. Technology is reshaping how insurers manage costs, serve members, and run their operations. In 2026, the global health insurance market is valued at USD 2.89 trillion, and it is expected to grow to USD 5.45 trillion by 2035, according to the Health Insurance Market Size report for 2026. At the same time, the insurtech market is booming. The industry is projected to reach USD 580 billion by 2033, growing at a compound annual growth rate of over 53%, as detailed in the Insurtech Market Size report.

For health executives, founders, and investors, keeping up with all these shifts is tough.

There is too much information and not enough focus. You need to cut through the noise to find the innovations that actually move the needle on costs, member satisfaction, and operational efficiency.

That is where this article helps. We provide a clear, data-backed look at the key technology trends reshaping private health insurance plans in 2026. These changes affect major players like CareFirst BCBS and United Healthcare, as well as smaller private insurance plans. We have already seen widespread AI adoption in health insurance, with over 94% of health plans adopting the technology.

If you want to stay ahead of these trends every day, consider getting clear daily AI updates from The Deep View Newsletter. It delivers practical insights that can help you make smarter decisions.

The Shifting Landscape of Private Health Insurance Technology

But understanding the big market numbers is only part of the story. The real transformation is happening underneath, where the technology backbone of private health insurance plans is being rebuilt from the ground up. For decades, most insurers relied on clunky legacy systems, old mainframes, and paper-heavy processes. Those systems made it hard to launch new products, personalize care, or even fix a billing error quickly.

That is changing fast in 2026. More and more insurance companies are moving to cloud-native, API-driven architectures. These modern platforms allow insurers to be agile. They can add new features, connect with digital health apps, and adjust benefits in real time.

Instead of waiting months to update a system, a single API call can now serve members faster. This shift is not just about speed. It is about personalization. When a member with a chronic condition needs care coordination, cloud-based systems can pull data from wearables, electronic health records, and pharmacy claims to tailor the experience.

The investment behind this change is enormous. According to the latest Insurance Platform Market Report, the global insurance platform market is expected to grow from $116.16 billion in 2025 to $207.52 billion by 2030. In the United States alone, over $1.5 billion has been poured into insurance platforms. Software companies that serve insurers, known as B2B SaaS firms, have captured nearly 40% of all insurtech investment. These funds are going straight into building better member portals, faster claims processing, and stronger fraud detection.

What is driving this urgency? Two big forces. First, regulatory changes are forcing insurers to open up their data and abide by new interoperability rules. Second, consumer expectations have shifted. People expect the same smooth digital experience they get from their bank or favorite online store. When they call united health care customer services or log into their CareFirst BCBS account, they want instant answers, not automated phone trees. This pressure is pushing every private insurance plans to adopt digital-first models or risk losing members.

Many health plans are also investing heavily in cybersecurity. With high-profile breaches affecting millions of records, protecting member data is now a top priority for executives. The shift to cloud-native systems does require strong security governance, but modern platforms actually offer better encryption and access controls than old legacy software.

In short, the infrastructure behind private health insurance plans is undergoing a once in a generation upgrade. Cloud and APIs are making insurers faster, more personal, and more secure. And that is just the beginning of what technology can do for the industry.

Key Drivers of Technology Adoption in Private Health Plans

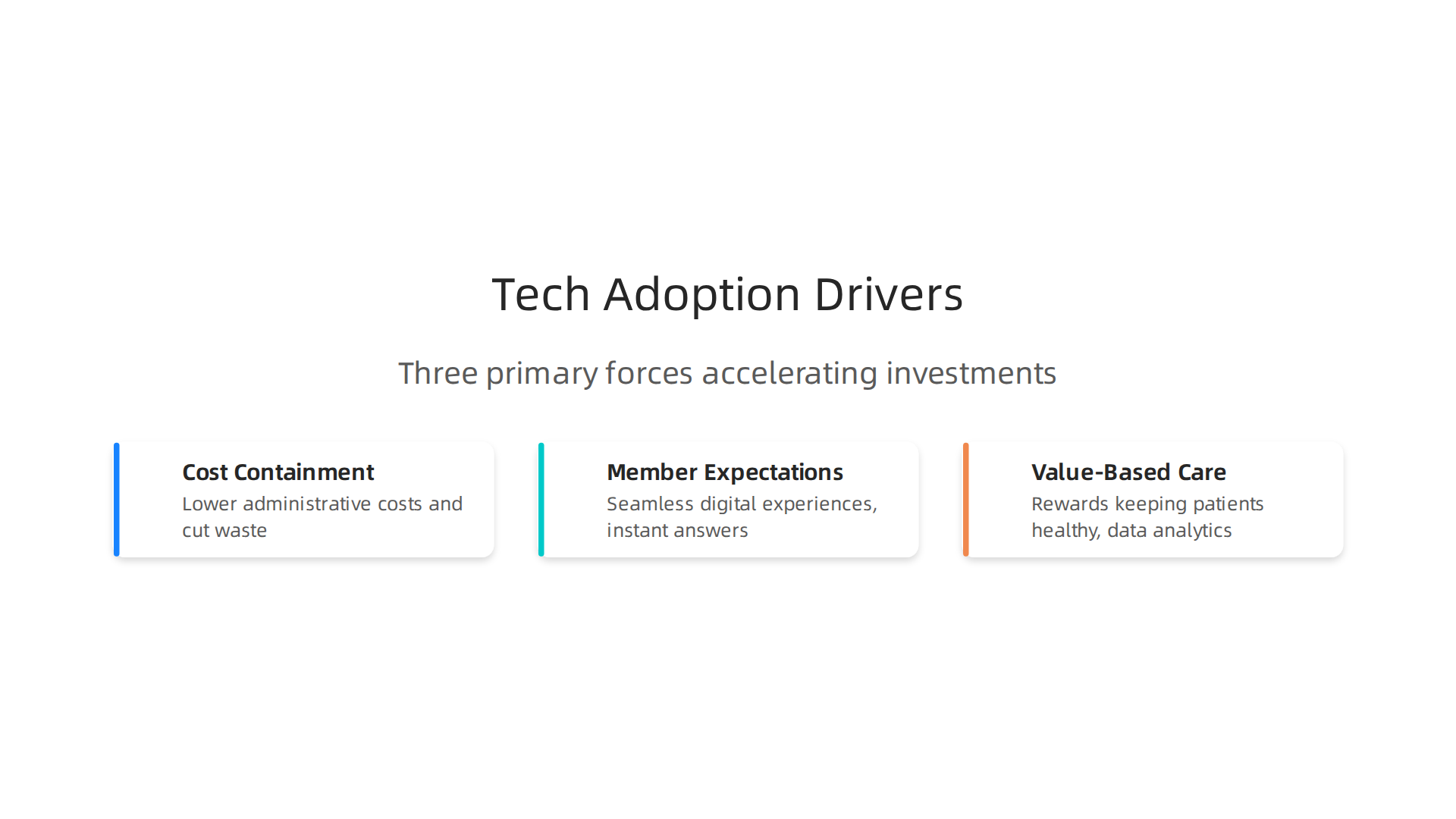

So what is pushing these massive technology investments? Three key drivers stand out.

First, cost containment. Insurers need to lower administrative costs and cut waste. AI claims processing and fraud detection tools help reduce overhead. The Insurtech Market Size report 2033 notes that AI and machine learning are now central to underwriting and claims automation, directly improving the bottom line.

Second, member expectations. People expect seamless digital experiences like they get from their bank. When they interact with their private health insurance plans, they want instant answers and mobile-friendly tools. This consumer demand is a powerful driver.

Third, value-based care. This model rewards keeping patients healthy. It requires advanced data analytics and interoperability. Many insurers are investing in these systems to coordinate care. For more on how health plans are adopting AI, see this article on AI adoption in health insurance.

These three forces are pushing every health plan to adopt technology faster. To stay updated on AI trends in healthcare, get the The AI Newsletter Worth Reading for daily insights.

Artificial Intelligence and Machine Learning

One area receiving major investment is artificial intelligence and machine learning. These technologies are already delivering measurable efficiency gains for private health insurance plans.

AI is transforming claims processing, fraud detection, and prior authorization. According to the NAIC briefing book on AI use, 84 percent of insurers now use AI, with half applying it to claims fraud detection. Machine learning models also improve risk stratification. The AI applications in health insurance from NIH notes that ML models now outperform traditional actuarial models, enabling better pricing and personalized plan recommendations.

Natural language processing powers intelligent virtual assistants. A AI survey from NVIDIA found that 37% of digital healthcare providers see virtual health assistants as their top ROI use case. These chatbots handle member questions and provide 24/7 support.

Private health insurance plans like CareFirst BCBS are using AI to speed up prior authorization. For more on how digital platforms are reshaping the industry, check out our article on digital health platforms in 2026.

Telehealth and Virtual Care Integration

Beyond AI, private health insurance plans are making virtual care a core part of their offerings.

They are expanding telehealth coverage and integrating it directly into member benefits. This shift matters because patients want convenient access. According to data on how telehealth use varies by physician specialty, over 71% of physicians used telehealth weekly in 2024, nearly triple pre-pandemic levels. Telehealth has become a standard care channel.

Technology platforms now enable seamless scheduling, billing, and data sharing between providers and payers. This reduces administrative friction and improves the member experience. As adoption grows, members expect user-friendly digital front doors from their insurance plans.

For health systems focused on improving patient handoffs, read our article on transitions of care in 2026. To stay updated on how AI is transforming these virtual care experiences, consider subscribing to The AI Newsletter Worth Reading.

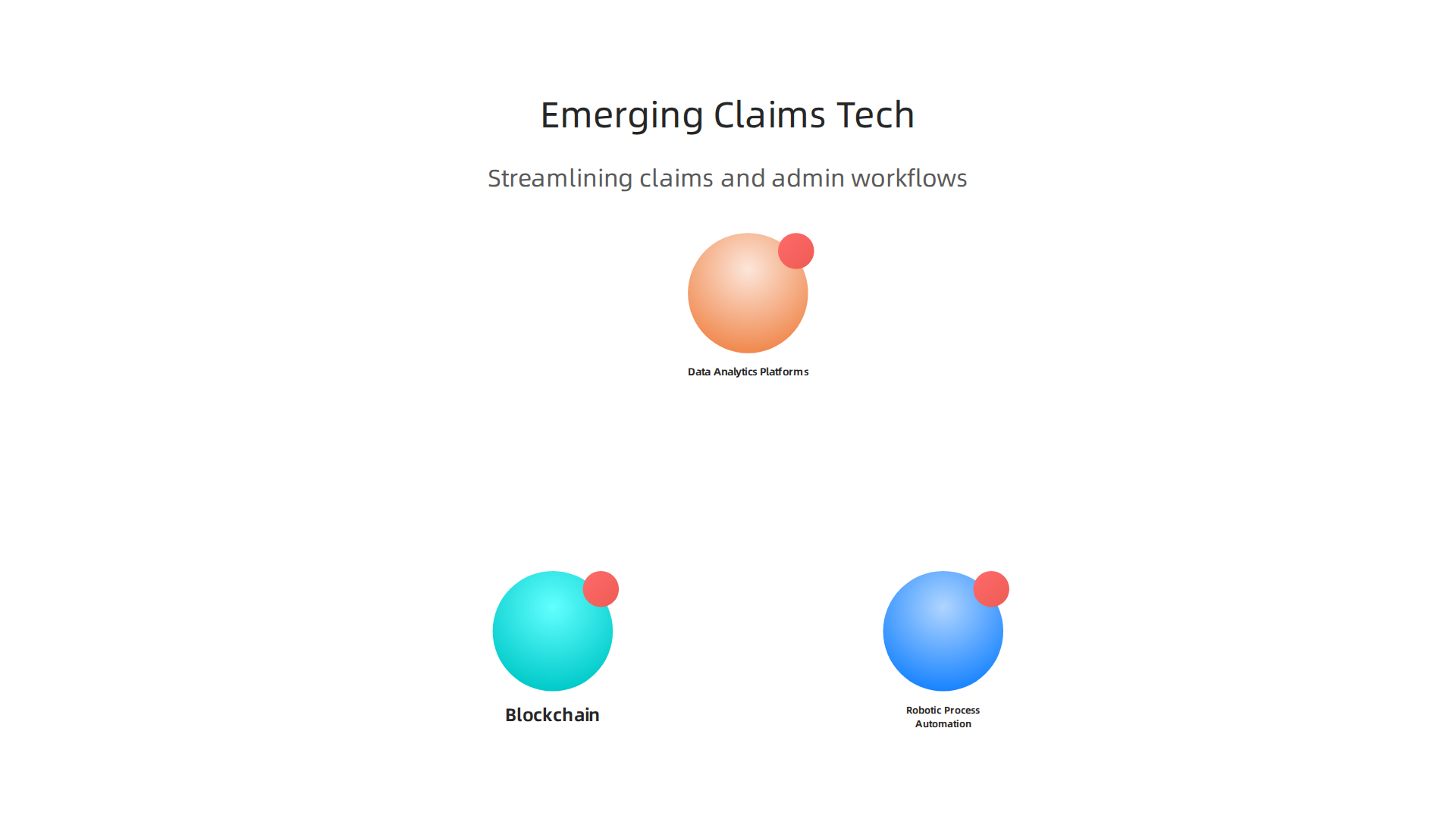

Emerging Technologies Reshaping Claims and Administration

While telehealth gets the spotlight, there is also a quiet revolution happening behind the scenes in claims processing and administrative workflows. Private health insurance plans are adopting new technologies to make these operations faster, cheaper, and more accurate.

From large national carriers to regional plans like CareFirst BCBS, the goal is the same: reduce costs and improve service.

Robotic process automation, or RPA, is one of the biggest game changers. RPA uses software bots to handle repetitive tasks like data entry, claim status checks, and payment posting. These bots work 24/7 and rarely make errors. Some systems cut processing time by up to 50%. For a busy insurance plan, that means claims get paid faster and staff can focus on harder problems. Customer service teams at plans like United Health Care have more time to handle complex member questions instead of chasing paperwork.

Blockchain is also starting to show up in the insurance world. While most people know blockchain from cryptocurrency, it has real uses for claims adjudication and provider network management. Blockchain creates a shared, tamper-proof record of transactions. This makes it easier to verify provider credentials, track claim submissions, and prevent fraud. Multiple parties can see the same data in real time without reconciliation delays. For private insurance plans with large provider networks, this alone can save millions each year in administrative overhead.

Data analytics platforms are another critical tool reshaping how plans operate. These systems scan large volumes of claim data to find patterns that humans would miss. They can flag unusual billing patterns that might mean fraud or simple errors. They also predict claim costs before they happen, which helps plans set better budgets and more accurate premiums. According to analyses on Eight Trends Shaping 2026 Healthcare Costs, AI documentation and coding tools are already increasing billing amounts across the industry. Payers are responding with their own data-driven strategies to manage spending and maintain financial stability. These platforms give plans the intelligence they need to stay ahead.

For private insurance plans, these technologies are not just nice to have. They directly impact the bottom line. Faster claims processing means happier providers and members. Better fraud detection saves millions. Smarter data analysis leads to more accurate pricing that protects both the plan and the patient. Best of all, these tools work together. RPA feeds clean data into analytics platforms. Analytics flags issues for human review. Blockchain keeps everything transparent and secure. It all adds up to a smoother, more efficient system that serves everyone better.

If you want to go deeper into how artificial intelligence is reshaping the insurance landscape, check out our article on why 94% of health plans are adopting AI in health insurance. It covers the key drivers behind this rapid adoption and what it means for the future of care.

How Private Health Insurance Plans Are Leveraging AI for Member Experience

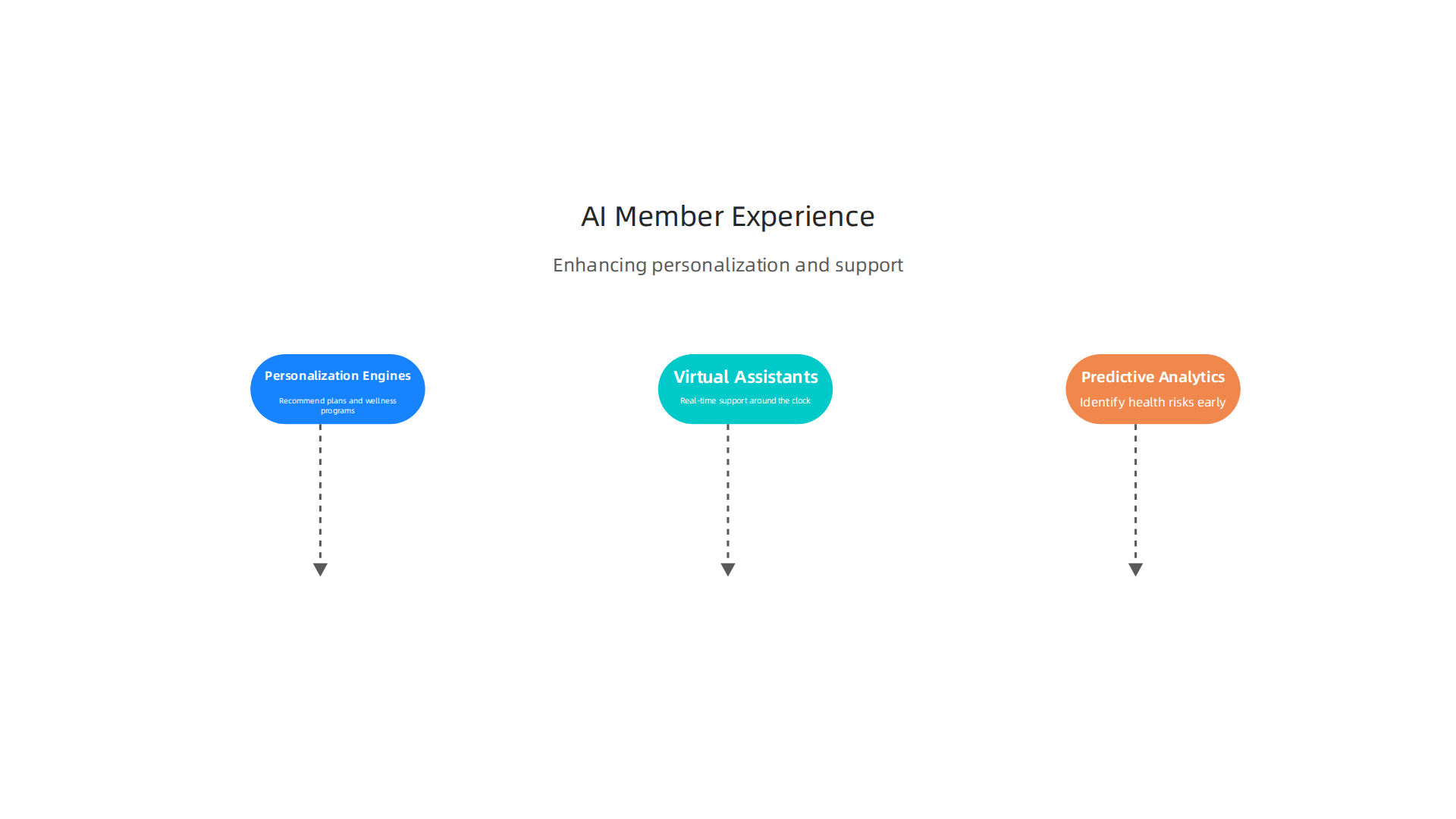

While back-office automation is important, private health insurance plans are also using AI to improve how members experience their coverage.

Personalization engines now recommend plans and wellness programs based on your unique health data. According to research on AI applications in health insurance, virtual assistants offer real-time support around the clock. These chatbots answer questions instantly and help boost satisfaction scores.

Predictive analytics go a step further. They identify health risks early and suggest preventive care options. This helps members stay healthier and reduces long-term costs.

For more on how health systems are transforming with technology, read about digital health platforms in 2026. Get clear daily AI updates from The Deep View Newsletter by subscribing to The AI Newsletter Worth Reading.

Chatbots and Virtual Assistants

Another big AI tool is the chatbot or virtual assistant. Many private health insurance plans now use these to handle your questions about benefits, claim status, or finding a doctor. They work 24/7, so you don’t have to wait on hold.

But today’s chatbots are smarter than old rule-based ones. They connect to your electronic health records (EHRs) and the insurer’s customer system. That means they understand your specific situation. For example, if a question gets too complex, the chatbot can hand you off to a real human agent. According to the NVIDIA survey on virtual health assistants and chatbots ROI, 37% of digital healthcare providers see chatbots as their top return on investment.

These advanced language models also cut down on hand-offs. They get your question right more often than older chatbots did. That means faster answers for you and fewer frustrated calls for everyone. For more on how technology is reshaping the back end of care, check out this guide on digital transformation in large health systems.

Personalized Plan Recommendations

Here is where AI really helps you as a member. When you shop for private health insurance plans, machines now look at your past claims, age, location, and even lifestyle habits from wearable devices. They can suggest the right coverage tier for your specific needs. This is much better than guessing which plan fits best.

Insurers also use smart nudges. They combine behavioral economics with AI to guide you toward cost-effective choices. For example, the system might suggest a lower premium plan with a health savings account if your data shows you rarely visit the doctor. These real-time suggestions happen during enrollment and annual plan selection.

The result? You feel understood and less overwhelmed. And health plans see better member retention. According to a 2026 briefing on AI use in health insurance, over 84% of insurance companies already use AI across their products. Many apply it to personalized plan matching and marketing. For a deeper look at this trend, check out this article on why 94% of health plans are adopting AI.

Want to stay ahead of these AI changes? The AI Newsletter Worth Reading delivers clear daily updates on how technology is reshaping healthcare and insurance.

The Role of Interoperability and APIs in Modern Health Insurance

While AI helps you pick the right plan, another powerful force works behind the scenes to make your insurance experience smoother. It is called interoperability. Think of it as a common language that lets different computer systems talk to each other. In healthcare and insurance, this language is often FHIR (Fast Healthcare Interoperability Resources).

FHIR-based APIs (application programming interfaces) allow insurers, doctors, and third-party apps to share data in real time. For people with private insurance plans, this means less paperwork and faster decisions. A big win is in prior authorization. That is the process where your doctor must get approval from your insurance before a procedure or medicine. It used to take days or even weeks. Now, with FHIR APIs, it can happen in hours.

A 2026 study on end to end prior authorizations using FHIR APIs found that over half of requests needed no authorization at all. And about 70% of submitted authorizations were automatically approved. The average time to get a decision dropped to just 26 hours. That is huge compared to the old days of waiting for days or weeks.

This kind of interoperability reduces administrative friction. Your doctor’s office spends less time on the phone with United Healthcare customer services or checking requirements for CareFirst BCBS. Instead, systems communicate automatically. The result is quicker care for you and lower costs for everyone.

Open API ecosystems also let health plans embed insurance features into other digital health tools. For example, a patient app could show your coverage details or check if a service needs prior approval. This creates a more connected experience. If you want to learn more about how technology is reshaping health systems, check out this article on how to modernize legacy health systems in regional hospitals.

The move toward open data and standard APIs is not just a trend. It is a requirement. New CMS rules now push health plans to adopt FHIR-based APIs by 2027. This means your private health insurance plans will keep getting smarter, faster, and easier to use.

Cybersecurity and Compliance: Protecting Sensitive Data in the Insurance Tech Stack

All this data sharing through APIs creates new risks. Health insurers are prime targets for cyberattacks because they hold a goldmine of protected health information (PHI). In 2025, the Change Healthcare ransomware attack affected roughly 190 million individuals, making it the largest healthcare breach in history. The average cost of a healthcare data breach in 2025 reached $7.42 million, the highest of any industry for the 14th year in a row, according to the Healthcare Data Breach Statistics report.

When you have a private health insurance plan, your personal and medical data must stay safe. That is where regulatory frameworks come in. HIPAA, state privacy laws, and new CMS rules demand strong security architectures. Insurers cannot just add cool tech features without locking down the data.

So what does good security look like in 2026? More health plans are adopting zero-trust models.

This means no user or system is trusted by default. Everyone must prove they are who they say they are, every time. AI-driven threat detection also helps spot unusual activity fast, before a breach spreads. And vendor risk management is becoming standard. Insurers must check the security of every outside company they work with.

Even small mistakes can lead to big problems. A misconfigured tracking tool or a weak vendor connection can expose millions of records. That is why compliance is not just a checkbox. It is a continuous process. If you want to dig deeper into how regulations shape health tech decisions, check out this article on Texas Medical Board regulations 2026 every health tech company must follow.

Staying ahead of threats means staying informed. For daily updates on how AI and technology are reshaping healthcare security, get clear insights from The AI Newsletter Worth Reading.

The bottom line: as your private insurance plans become more digital, the companies behind them must work hard to earn and keep your trust. Strong cybersecurity is now a core part of the insurance tech stack, right alongside AI and APIs.

The Future of Value-Based Care and Payment Technology

Now let us look at where all this technology is heading. The biggest shift in private health insurance plans right now is the move toward value-based care. Instead of paying for every test or procedure, insurers pay for outcomes. A healthier patient means lower costs for everyone.

This sounds simple, but it requires serious data power. Technology platforms now pull together clinical records, claims history, and even social factors like housing or food access. With all that information in one place, insurers can do accurate risk scoring. They can see which members need extra support before a costly emergency happens. This is population health management in action.

Regulations are pushing this forward too. The CMS Interoperability and Prior Authorization Final Rule requires plans to use FHIR-based APIs. This rule is designed to support the move toward value-based payment models by making data flow more freely between providers and payers.

Alternative payment models like bundled payments and capitation are becoming more common. These models depend on advanced analytics and real-time reporting. Insurers need to know instantly how their members are doing. Without good data, these payment models fall apart. That is why technology is not optional anymore.

Looking ahead, blockchain and smart contracts may automate value-based payment reconciliation. Instead of waiting weeks for claims to process, payments could happen automatically when certain health outcomes are met. This would save administrative time and reduce errors.

For members of plans like CareFirst BCBS or anyone contacting United Health Care customer services, this shift means faster approvals and less paperwork. For a deeper look at how AI is driving these changes, check out this article on health insurance AI trends.

The technology is getting smarter. The goal is to make private insurance plans work better for people, not just for billing departments.

Conclusion

We have covered a lot of ground. From AI tools that speed up claims to telehealth platforms that connect patients with doctors, the world of private health insurance plans is changing fast. Interoperability rules now force data to flow more freely. Cybersecurity keeps member information safe. And value-based care is pushing insurers to focus on outcomes instead of volume.

So what does all this mean for decision-makers?

The message is clear. You need to invest in technology that is modular, secure, and built around the member experience. The days of clunky legacy systems are numbered. Patients expect fast, easy, and safe care. Private insurance plans must meet those expectations or risk falling behind.

The trends we discussed are grounded in the latest data and expert perspectives. Staying agile is the only way forward. Prioritize innovation that drives measurable outcomes.

One easy way to keep up with all these changes is to subscribe to The AI Newsletter Worth Reading. It cuts through the noise and gives you clear daily AI updates that actually matter for health tech.

And if you want to see how technology is reaching underserved communities, read this article on how community health technology is reaching underserved communities in 2026.

The future of private insurance plans is about people first, technology second. But you need the right tech to make it all work.

Summary

This article explains the key technology trends reshaping private health insurance plans in 2026 and why they matter for executives, founders, and investors. It covers market context and the move away from legacy mainframes toward cloud-native, API-driven platforms that enable faster product updates, personalized care, and stronger security. You’ll read how AI and machine learning are speeding claims, detecting fraud, powering virtual assistants, and improving plan recommendations, while telehealth, RPA, blockchain, and data analytics streamline operations and cut costs. The piece also explains how FHIR-based interoperability is shortening prior authorization times and enabling value-based payment models, and why zero-trust cybersecurity and vendor governance are now essential. By the end, readers will understand which technologies drive measurable savings and member satisfaction and how to prioritize modular, secure investments that support outcomes-based care.