Introduction

Medical debt is not just a personal financial burden. It is a system-wide crisis that touches nearly every corner of the U.S. healthcare industry. Right now, about 20 million people in the United States owe medical debt, with total obligations reaching at least $220 billion according to the Survey of Income and Program Participation. That is a staggering number. And it is growing.

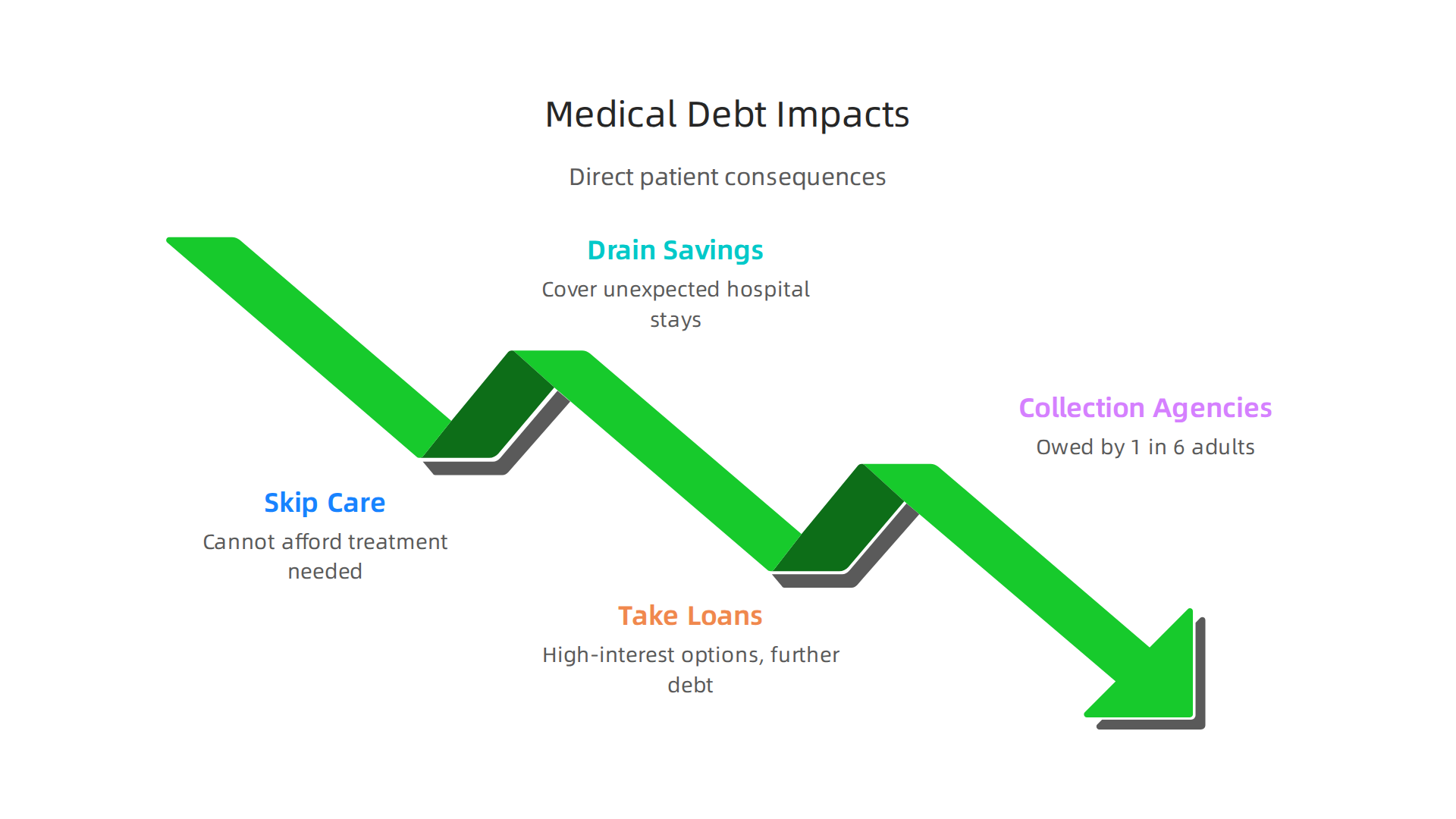

Nearly one in 12 adults carries this weight. Many of them are skipping care they need because they cannot afford it.

Others are draining savings or taking on high-interest loans just to cover unexpected hospital stays. The consequences ripple out from individual patients to entire health systems struggling with bad debt, delayed payments, and shrinking margins.

But here is the thing. In 2026, we finally have better tools to fight this problem. Financial technology solutions including AI-driven billing systems, smarter revenue cycle management, and targeted efforts like the rip medical debt movement are giving hospitals and patients new ways to reduce the financial damage. These innovations are not just about collecting money faster. They are about preventing debt from forming in the first place and clearing it when it does.

For health tech executives, investors, and decision-makers, understanding how these tools work is no longer optional. It is essential.

This article gives you an evidence-based roadmap. We will look at what the data shows about medical debt today, how technology is changing the game, and what smart leaders are doing to protect both their patients and their bottom lines.

If your organization is ready to explore new approaches to innovative primary care and senior care models, the lessons in this guide will help you connect the dots between financial health and clinical outcomes.

Subscribe Free to stay ahead of the trends shaping healthcare innovation.

The Medical Debt Crisis in 2026: Scale, Impact, and the Role of Fintech

To understand why tools like rip medical debt programs are gaining so much attention, you first need to see just how big this problem really is. The numbers are sobering. And in 2026, they are getting worse, not better.

Right now, about 20 million people in the United States owe medical debt. That is nearly one in 12 adults. And the total amount owed sits at least at $220 billion according to the Survey of Income and Program Participation. But here is the thing. Some researchers believe that number is actually much higher. A Stanford analysis even suggests the commonly cited $81 billion figure greatly underestimates the real crisis.

Medical debt remains the leading cause of bankruptcy in the U.S. It does not hit everyone equally either. Low-income households and minority communities carry a much heavier load. A 2022 KFF report found that about four in ten adults (41%) reported having debt due to medical or dental bills. And for uninsured people, the rate jumps to 23%.

The COVID-19 pandemic made everything worse. Rising healthcare costs pushed more families into financial trouble. Many people delayed care during the pandemic, and now they are facing larger, more urgent health problems that cost even more to treat. A 2026 report from the Commonwealth Fund warns that these pressures will likely intensify as enhanced Affordable Care Act premium tax credits expire.

So what happens when people cannot pay? They skip care. They drain savings. They take out loans. Some even turn to high-interest credit cards or collection agencies.

One in six adults now reports debt owed to a bank or collection agency from loans taken to cover medical bills. This cycle of debt hurts both patients and the health systems trying to serve them.

This is where technology steps in. RCM healthcare (revenue cycle management) tools are changing how hospitals handle billing and collections. Instead of sending confusing paper bills that patients ignore, modern fintech systems offer clear payment plans upfront. Some use AI to identify patients who qualify for financial assistance before their bills go to collections. Others automate charity care applications so fewer people fall through the cracks.

These tools also make debt forgiveness more practical. Hospitals using smart rip medical debt programs can identify large pools of qualifying debt and clear it in bulk at pennies on the dollar. That helps patients get back on their feet, and it cleans up the health system’s books at the same time.

For decision-makers, the takeaway is clear. The old way of handling medical billing and collections is broken. Fintech offers a path forward that reduces administrative overhead, improves payment transparency, and enables forgiveness models that actually work. If your organization is ready to explore these approaches within broader care models, you can find more in our coverage of innovative primary care tech and models reshaping senior care in 2026.

Subscribe Free to get clear daily AI updates and stay ahead of the trends shaping healthcare innovation.

Understanding ‘RIP Medical Debt’ and the Rise of Medical Debt Relief Platforms

You now know the scale of the medical debt crisis. So how do you actually start fixing it? The answer starts with a simple but powerful idea: buying debt at a discount and forgiving it.

That is exactly what the organization originally called RIP Medical Debt set out to do. Founded in 2014 by former collections industry professionals, the nonprofit figured out that hospitals and collection agencies often sell old debt for pennies on the dollar. So instead of letting patients suffer under those bills, the organization used donations to buy that debt and simply forgive it.

The impact has been massive. As of February 2026, the organization now known as Undue Medical Debt has relieved debts for over 15.21 million people, totaling more than $25.4 billion. In 2024, the group officially updated its name from RIP Medical Debt to Undue Medical Debt to better reflect its mission. The core model stayed the same: use donated funds to buy bundled medical debt at steep discounts and erase it for financially vulnerable families.

This approach works because of how medical debt gets sold. Hospitals bundle thousands of old accounts and sell them to buyers for a fraction of face value. When Undue Medical Debt buys one of those bundles, they can forgive the entire balance of every account inside it. For every dollar donated, the organization can erase many times that amount in debt.

But here is the thing. The landscape in 2026 has moved well beyond the original model. Newer fintech platforms now build directly on top of this idea, and they go much further. These platforms use AI-powered tools to identify patients who qualify for financial assistance before their bills ever go to collections. They automate charity care applications. They offer integrated payment plans so patients can resolve bills without falling into new debt cycles.

For health systems, the math works well. Instead of writing off debt entirely, they can partner with relief platforms and recover a portion of receivables while giving patients a clean slate. Some states are even requiring this. North Carolina passed a medical debt relief plan that requires hospitals to enter into an agreement with Undue Medical Debt or another vendor by March 2025.

These partnerships do more than clean up balance sheets. They rebuild trust with the community. Patients who receive unexpected debt forgiveness are more likely to return for care instead of avoiding it. That is better for health outcomes and better for the health system’s bottom line.

The takeaway is straightforward. The rip medical debt model works, and the technology around it keeps getting smarter. Health systems that want to reduce administrative overhead and improve patient relationships should pay close attention. Many of these tools now integrate with rcm healthcare workflows, making adoption smoother than ever.

If your organization is evaluating how to handle medical debt more humanely, start by looking at how relief platforms identify qualifying accounts. The best solutions combine aggressive debt forgiveness with proactive outreach so no eligible patient slips through the cracks. Subscribe Free to get clear daily AI updates and stay ahead of the trends shaping healthcare innovation.

Key Financial Technology Solutions for Healthcare Payments

Now that you understand how the rip medical debt model works, the next question becomes: what tools can actually help health systems put this into practice?

The good news is that financial technology has caught up with the problem. Several new solutions are making it easier for hospitals to reduce patient balances, improve cash flow, and avoid the cycle of debt altogether.

AI-Powered Billing and Coding Automation

One of the biggest reasons patients end up with unexpected medical bills is simple human error. Coding mistakes and mismatched insurance data lead to denied claims. Those denials then get billed back to the patient.

AI-powered billing and coding tools fix this. They check claims before they are even submitted. They find errors, flag missing information, and suggest corrections. The result is fewer denials and faster reimbursement.

For health systems, this directly lowers patient balances. When claims get paid correctly the first time, there is less left over for the patient to fight about. These tools also integrate smoothly with rcm healthcare systems, making adoption easier for existing teams.

If you work with senior populations, you might also want to see how innovative primary care tech models are reshaping senior care in 2026. Many of the same AI tools help manage complex billing for older adults.

Buy Now, Pay Later for Medical Expenses

The phrase "buy now, pay later" usually makes you think of online shopping. But in 2026, this model is gaining real traction in healthcare.

Medical BNPL platforms offer patients zero-interest installment plans for their out-of-pocket costs.

Instead of getting a single huge bill that forces them into credit card debt, patients split the cost into manageable monthly payments.

This is a game changer. According to a 2026 report from Zurich, healthcare events are now a major source of financial stress, forcing people to rely on debt or drain savings just to access care. BNPL options give patients a way to stay current without ruining their credit.

For health systems, the benefit is clear. Patients who use BNPL are far less likely to default. That means fewer accounts go to collections, which reduces the burden on your administrative team.

Blockchain-Based Claims Processing

Blockchain sounds like a buzzword, but in healthcare payments, it actually solves a real problem: trust.

Claims processing today involves multiple parties. Hospitals, insurers, and third-party payers all handle the same data. This creates opportunities for fraud, duplicate billing, and simple mistakes.

Blockchain creates a single, tamper-proof record of every claim. Everyone sees the same information. Nobody can change it after the fact. This reduces fraud, speeds up dispute resolution, and builds trust between payers and providers.

States are already pushing for better transparency. The Commonwealth Fund noted in early 2026 that pressures generating medical debt are likely to intensify as federal protections stall. Blockchain tools help health systems stay ahead of these changes by proving every transaction is honest.

What This Means for Your Organization

The tools exist right now. AI fixes billing errors before they happen. BNPL gives patients a fair way to pay. Blockchain makes the whole system more transparent.

When you combine these with the rip medical debt relief model, you get a complete approach. You prevent new debt from forming. And for the debt that already exists, you have a proven way to erase it.

Health systems that adopt these technologies now will be the ones patients trust in the years ahead.

Want to stay ahead of the trends shaping healthcare innovation? Subscribe Free to get clear daily AI updates delivered straight to your inbox.

How Health Systems Are Implementing Fintech to Reduce Bad Debt

The technology is ready. But how do actual hospitals and health systems put it to work in 2026?

It is one thing to read about AI billing tools and buy now, pay later plans. It is another thing to integrate them into real daily operations. Here is what the leaders are doing right now.

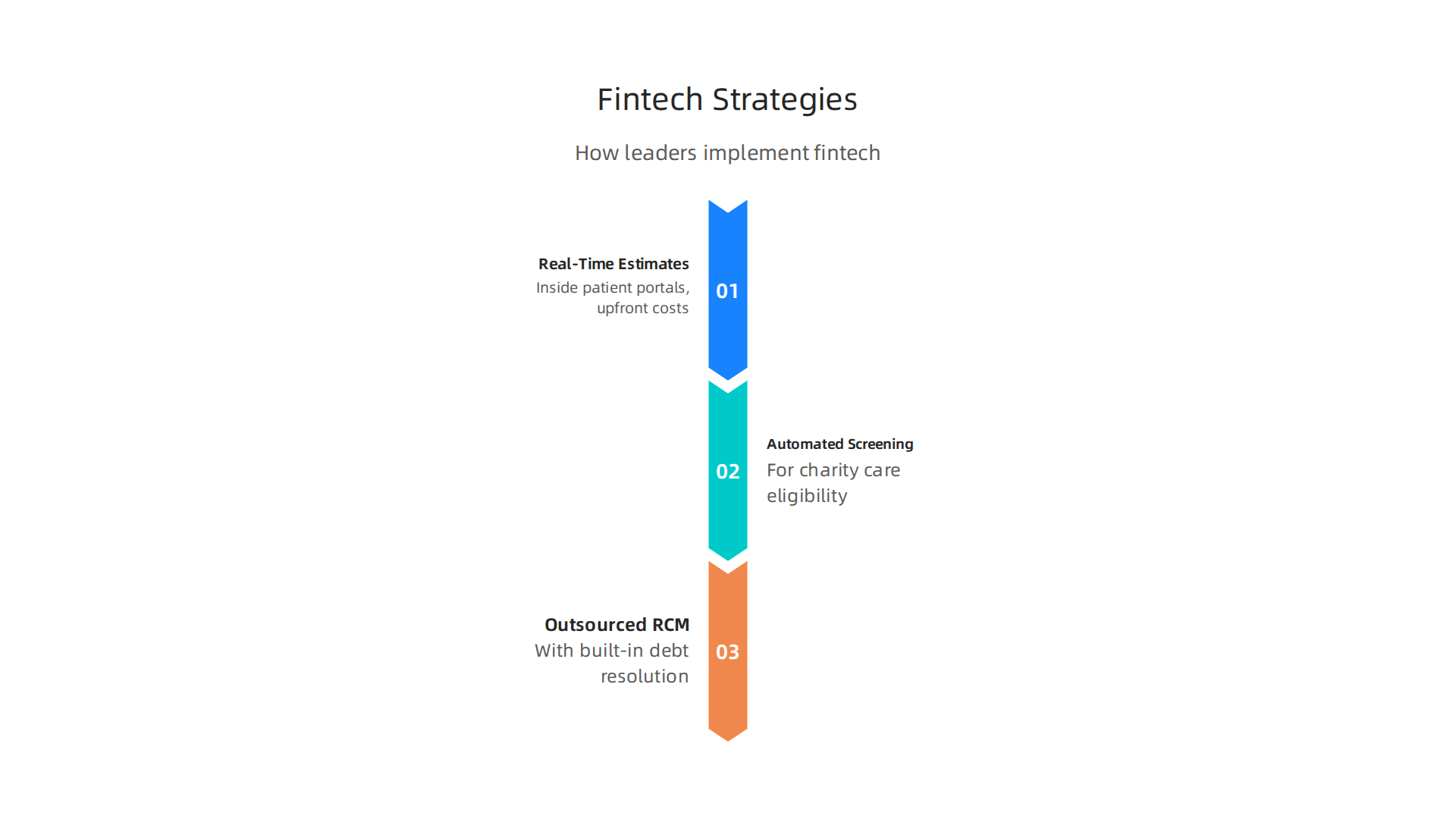

Real-Time Cost Estimates Through Patient Portals

The first big shift is happening inside patient portals.

Hospitals are now embedding fintech APIs directly into the patient experience. When a patient logs in to check their lab results or schedule a follow-up, they see real-time cost estimates before any procedure. They can also set up payment plans on the spot.

This changes everything. Instead of getting a surprise bill weeks later, patients know what they owe upfront. And they can choose a plan that fits their budget. This approach helped LifeBridge Health reduce their bad debt by 20 percent using better digital engagement, according to a case study from Flywire.

When patients see realistic prices and manageable payment options, they are far less likely to default. That means fewer accounts ever make it to collections.

Automated Charity Care Screening

Here is the thing: many patients qualify for financial assistance but never apply. The process is confusing. The forms are long. So they just ignore the bill until it becomes a problem.

Smart health systems are fixing this with automation. Instead of waiting for patients to ask for help, the system checks eligibility behind the scenes. Before accounts ever go to collections, the software flags patients who qualify for charity care and enrolls them automatically.

As the AcademyHealth blog noted in March 2026, hospitals can reduce the harms of medical debt by better leveraging their existing financial assistance programs. The key is making the process invisible to the patient. They simply get a smaller bill or no bill at all.

This is especially important for senior patients who may be relying on john hancock long term care policies or other insurance to cover their needs. Automated screening makes sure they get every benefit they have earned. If you work with older adults, you might want to see how innovative primary care tech models are reshaping senior care in 2026.

Outsourced RCM with Built-In Debt Resolution

The third trend is outsourcing. More health systems are handing their revenue cycle management over to specialized firms that include fintech-powered debt resolution in the package.

These are not your old-school collections agencies. They are rcm healthcare partners that use data to find the best path for each patient. Some offer forgiveness programs. Others use settlement tools. And many now connect directly to Undue Medical Debt (formerly RIP Medical Debt) to bulk-erase qualifying debt.

This matters because the nonprofit has already relieved over $25.4 billion in medical debt for more than 15 million people as of February 2026, according to Wikipedia. Hospitals that partner with them can wipe out large pools of bad debt at a fraction of the cost.

Some patients also protect themselves with term life insurance to cover final expenses. But for the living, medical debt relief programs offer immediate help.

The Bottom Line

Health systems that adopt these three strategies are seeing real results. Fewer denials. Happier patients. Less bad debt on the books.

The rip medical debt model is not just a charity effort anymore. It is becoming a core part of how smart hospitals manage their finances.

Want to stay ahead of the trends shaping healthcare innovation? Subscribe Free to get clear daily AI updates delivered straight to your inbox.

The Regulatory Landscape for Medical Debt and Fintech (HIPAA, CFPB, State Laws)

So health systems are rolling out these cool fintech tools. But here is the tricky part. Every new payment system, every automated screening tool, every debt resolution partner has to play by a bunch of rules.

And those rules are shifting fast in 2026.

The CFPB Roller Coaster

The Consumer Financial Protection Bureau has been trying hard to keep medical debt off credit reports. In January 2025, the CFPB finalized a rule that would have banned credit reporting agencies from including medical bills in consumer reports. That was a big win for patients.

But then a federal court vacated that rule in August 2025. A judge in Texas said the CFPB overstepped. So today, the federal protection that was supposed to keep medical debt out of credit reports is gone. The three major credit bureaus (Equifax, Experian, TransUnion) still removed some medical debt voluntarily, but the legal requirement is no longer in place. You can read more about what happened in this detailed explainer from AAPD.

This means health systems and fintech companies cannot assume federal protection is coming. They have to build their own compliance strategies.

State Laws Are Filling the Gap

With the federal rule gone, states are stepping up. In 2025 alone, six states (Delaware, Maine, Maryland, Oregon, Vermont, and Washington) passed laws that restrict how medical debt shows up on credit reports. Other states are considering similar moves. The result is a patchwork. A fintech tool that works perfectly in one state might break the rules in another.

For example, seniors are especially vulnerable to medical debt. If you work with older adults, you might be interested in how innovative primary care tech models are reshaping senior care in 2026. These models also have to comply with state-level protections for patients who rely on insurance like john hancock long term care policies.

HIPAA Never Takes a Vacation

Every fintech that touches patient data has to follow HIPAA. That includes payment portals, automated screening tools, and any rcm healthcare software handling protected health information. One slip can lead to fines and loss of trust.

The key is making sure the technology partner you choose is HIPAA compliant from day one. That is not optional. It is the law.

What This Means for You

The regulatory landscape is messy. But that does not mean you should wait. Smart health systems are moving forward with fintech solutions that respect patient privacy and adapt to state laws. Some also partner with organizations like RIP Medical Debt (now Undue Medical Debt) to wipe out old debt quickly, a strategy often called rip medical debt.

The rules will keep changing. The best way to stay informed is to get easy daily updates. Subscribe Free to The Deep View newsletter for simple, clear insights on AI and healthtech regulation.

Strategic Takeaways for Health Tech Executives and Investors

Now that you understand the shifting rules, let’s talk about what this means for your strategy. The message is simple: fintech is no longer just a back-office cost. It’s a strategic asset that can drive patient loyalty and keep your organization financially healthy.

From Cost Center to Strategic Asset

Too many health systems still see payment technology as an expense. But the data tells a different story. The global healthcare patient financing platform market was valued at $7.94 billion in 2025 and is on track to reach $28.15 billion by 2035. That is massive growth. And it signals something important: patients expect modern, flexible payment options.

Hospitals that adopt digital engagement tools see real results. LifeBridge Health, for example, reduced its bad debt by 20 percent after implementing a digital patient payment platform. That is not just a nice feature. It is a direct boost to the bottom line.

What Investors Should Look For

If you are an investor in health tech, the opportunity is real. But not every platform is worth backing. Focus on three things:

- Clear ROI. Does the solution show measurable reductions in bad debt or improvements in patient collections?

- Regulatory compliance. With the CFPB rule vacated and state laws multiplying, a platform must be built to adapt. Check out this summary of what rules apply in 2026 for a quick overview.

- Scalable patient engagement. Can the tool work across different health systems and patient populations? Solutions that integrate with existing rcm healthcare systems are a strong bet.

Remember, patients are people with different financial realities. Some rely on products like john hancock long term care insurance or term life insurance to manage future health costs. A good fintech platform helps them use those resources wisely without adding stress.

Early Movers Win

Health systems that jump on fintech now will stand out in a crowded market. Patients remember how you made them feel about their bill. A clear, fair, and easy payment experience builds trust. It also attracts top talent who want to work for innovative organizations.

One smart move is to pair your payment tools with a debt relief partnership. Some health systems work with Undue Medical Debt (you might still hear it called rip medical debt). This strategy lets you erase old debt quickly, which reduces patient anxiety and improves health outcomes.

The regulatory landscape will keep changing. But that is no reason to wait. Start building your fintech strategy today. To keep up with the latest trends in healthtech and fintech regulation, Get Free Updates from The Deep View newsletter.

Summary

This article examines the scale of the U.S. medical debt crisis in 2026 and shows how new financial technologies and debt-relief models are changing the rules. It explains the original RIP Medical Debt approach (now Undue Medical Debt), how buying bundled accounts at deep discounts can erase obligations, and how contemporary fintech — from AI billing and BNPL to blockchain — prevents bills from forming and speeds resolution. The guide covers practical hospital tactics like real-time cost estimates, automated charity-screening, and outsourced RCM with built-in debt resolution, while also mapping the shifting regulatory landscape around HIPAA, CFPB, and state laws. Readers will learn which tools produce measurable reductions in bad debt, how to evaluate vendors for ROI and compliance, and strategic steps executives and investors can take to protect patients and improve financial performance. The piece balances policy context, technology choices, and implementation lessons so decision-makers can act now to reduce patient harm and strengthen their organizations.